Lebensversicherung:Ist es eine kluge Investition? Die Fakten verstehen

Es gibt mehr als 400.000 Versicherungsmakler in diesem Land und fast alle von ihnen würden Ihnen gerne eine Lebensversicherung verkaufen. Wenn Sie eine Police mit Prämien von 40.000 US-Dollar pro Jahr abschließen, liegt die Provision für diesen Agenten normalerweise zwischen 20.000 und 44.000 US-Dollar. Wie Sie sich vorstellen können, kann diese Provision sehr motivierend sein, insbesondere angesichts des durchschnittlichen Einkommens eines Versicherungsvertreters von 49.840 US-Dollar. Erschwerend kommt hinzu, dass viele der schlechtesten Policen die höchsten Provisionen bieten. Leider wird die überwiegende Mehrheit der verkauften Policen unsachgemäß verkauft und die überwiegende Mehrheit derjenigen, die sie verkaufen, sind Verkäufer, die sich als Finanzberater ausgeben.

Als Folge dieses lächerlichen Interessenkonflikts verbreiten Agenten oft ernste Mythen, um Sie zum Kauf ihres Produkts zu bewegen. Dies könnte die vernichtende Statistik erklären, dass mehr als 80 % derjenigen, die dieses Produkt kaufen, es vor ihrem Tod loswerden, und Umfragen unter echten Ärzten auf dieser Website und in unserer Facebook-Gruppe zeigen, dass die überwiegende Mehrheit derjenigen, die Lebensversicherungen abgeschlossen haben, ihren Kauf bereuen. Wenn Ihnen das alles neu ist, dann lesen Sie „Alles, was Sie über eine Lebensversicherung wissen müssen“, bevor Sie mit diesem Beitrag fortfahren.

Während die meisten WCI-FB-Gruppenmitglieder noch nie eine Lebensversicherung abgeschlossen haben, bereuen es 76 % derjenigen, die dies getan haben.

Laden ...

Die Zahlen sind ähnlich, aber etwas niedriger in der laufenden Umfrage auf dieser Website (die im Gegensatz zur FB-Gruppe die Abstimmung durch diejenigen zulässt, die diese Policen verkaufen).

Viele Leute denken, ich hasse Lebensversicherungen. Das tue ich eigentlich nicht. Ich hasse die Art und Weise, wie es verkauft wird, und diejenigen, die es unangemessen verkaufen. Wenn Sie wirklich verstehen, wie es funktioniert, und es trotzdem wollen, können Sie gerne so viel kaufen, wie Sie möchten. Es berührt mich wirklich nicht auf die eine oder andere Weise. Aber ich habe es satt, auf Leser und Zuhörer zu stoßen, die beim Kauf NICHT verstanden haben, wie es funktioniert, und die es dann NICHT wollen, wenn sie es verstehen.

So funktioniert eine Lebensversicherung

Eine Lebensversicherung kann auf viele verschiedene Arten abgeschlossen werden, im Allgemeinen zahlen Sie jedoch eine monatliche oder jährliche Prämie für einen bestimmten Zeitraum oder bis zu Ihrem Tod. Je länger der Zeitraum ist, über den Sie die Prämien zahlen, desto niedriger sind die Prämien. Wenn Sie sterben, erhält Ihr Begünstigter den Erlös aus der Police. Da bei jeder Lebensversicherung die Auszahlung garantiert ist, wenn Sie sie bis zu Ihrem Tod behalten, sind die Prämien viel höher als bei einer vergleichbaren Risikolebensversicherung.

Eine Lebensversicherung ist, wie andere Arten von dauerhaften Lebensversicherungen auch, eine Mischung aus Versicherung und Kapitalanlage. Der Barwert der Police erhöht sich im Laufe der Jahre. Dieser Barwert wächst steuergeschützt, und Sie können sich das Geld dort sogar steuerfrei (aber nicht zinsfrei) leihen. Bei Ihrem Tod wird der von Ihnen geliehene Betrag (zuzüglich der Zinsen) von der Sterbegeldleistung abgezogen und der Rest an Ihren Anspruchsberechtigten ausgezahlt. (Sie erhalten den Barwert oder die Sterbegeldleistung, nicht beides.)

Dieser Anlageaspekt ermöglicht es denjenigen, die Lebensversicherungen verkaufen, alle möglichen kreativen Gründe für den Kauf und kreative Möglichkeiten zu finden, sie zu strukturieren. Die extremsten Befürworter könnten sogar argumentieren, dass Sie während Ihres gesamten Lebens KEINE anderen Finanzprodukte benötigen, da eine Lebensversicherung offenbar alle Ihre Bedürfnisse abdecken kann, einschließlich Hypotheken, Verbraucherkredite, Versicherungen, Investitionen, Ersparnisse für das Studium und Ruhestand.

Das Problem besteht darin, dass es für jeden Einsatz einer Lebensversicherung in der Regel eine bessere Möglichkeit gibt, mit diesem finanziellen Problem umzugehen. In diesem Beitrag werden die 38 häufigsten Mythen über die Lebensversicherung aufgeführt, die von ihren Befürwortern verbreitet werden.

Mythos Nr. 1 – Das ganze Leben ist gut für die Absicherung des Vorruhestandseinkommens

Eine Risikolebensversicherung ist nicht der beste Weg, um Ihr Einkommen zu schützen, eine Risikolebensversicherung hingegen schon. Bevor Sie in den Ruhestand gehen, können Sie eine günstige Risikolebensversicherung abschließen, um für den Fall Ihres vorzeitigen Todes für Ihre Lieben zu sorgen. Eine 30-jährige Risikolebensversicherung mit Prämie und einem Nennwert von 1 Million US-Dollar, die von einem gesunden 30-Jährigen gekauft wird, kostet 680 US-Dollar pro Jahr. Eine ähnliche Lebensversicherung kostet mehr als das Zehnfache, nämlich 8.000 bis 10.000 US-Dollar pro Jahr. Das ist Geld, das nicht für Hypothekenzahlungen oder Urlaube ausgegeben oder für den Ruhestand investiert werden kann.

Mythos Nr. 2 – Das ganze Leben ist der beste Weg, eine dauerhafte Sterbegeldleistung zu erhalten

Das ganze Leben ist nicht der beste Weg, um eine dauerhafte Sterbegeldleistung zu erhalten – das garantierte universelle Leben ohne Verfall ist es. Es gibt einige wenige Menschen, die eine Versicherungspolice benötigen oder wollen, die bei ihrem Tod, wann immer dieser eintritt, die Auszahlung übernimmt. Dies kann bei einigen ungewöhnlichen Problemen bei der Nachlassplanung hilfreich sein. Es gibt jedoch ein besseres Produkt, das dies bietet und viel günstiger ist als eine Lebensversicherung. Es heißt Garantierte, ausfallsichere, universelle Lebensversicherung . Es wird KEIN Barwert angesammelt, sondern lediglich eine lebenslange Sterbegeldleistung gewährt. Sie kostet nur halb so viel wie eine Lebensversicherung, Sie werden also nicht überrascht sein, wenn Sie erfahren, dass die Provision des Maklers für diesen Verkauf weitaus niedriger ausfällt.

Nennen Sie mich zynisch, aber ich vermute, das könnte einer der Gründe sein, warum Sie noch nie von einem garantierten universellen Leben ohne Fehler gehört haben. Die Lebensversicherung bietet eine garantierte Sterbegeldleistung, die PROJEKTIEREND (jedoch nicht garantiert) langsam ansteigt, so dass Sie, wenn Sie innerhalb Ihrer Lebenserwartung oder später sterben, etwas mehr als die ursprüngliche Sterbegeldleistung der Police zurücklassen.

Sterbegeld und Inflation

Eine lebenslange Lebensversicherung, die ich mir kürzlich angesehen habe, ging davon aus, dass die Sterbegeldleistung einer 1-Millionen-Dollar-Versicherung, die mit 30 Jahren gekauft wurde, bei Tod im Alter von 83 Jahren 3,17 Millionen US-Dollar betragen würde. Das klingt großartig, fast wie ein Inflationsschutz der Sterbegeldleistung. Abgesehen davon, dass die historische Inflation etwa 3,1 % beträgt. Bei 3,1 % entspräche 1 Million US-Dollar jetzt 5,04 Millionen US-Dollar in 53 Jahren. Eine Lebensversicherung würde durch eine unerwartete Inflation zerstört, da die Dividenden in erster Linie durch nominale Anleihen gedeckt sind, deren Werte in einem Umfeld mit hoher Inflation vernichtet würden.

Daher ist eine Risikolebensversicherung weder der beste Weg, um eine garantierte lebenslange nominelle Sterbegeldleistung noch eine garantierte lebenslange tatsächliche Sterbegeldleistung zu gewährleisten. Wofür ist es also gut? Wie wäre es mit einer garantierten Sterbegeldleistung, die sich erhöhen könnte, wenn die Versicherungsgesellschaft sie erhöhen möchte? Wären Sie bereit, dafür doppelt so hohe Prämien zu zahlen? Das habe ich nicht gedacht.

Mythos Nr. 3 – Eine Lebensversicherung bietet eine großartige Kapitalrendite

Das ganze Leben ist nicht die beste Art zu investieren – traditionelle Investitionen schon. Wenn Sie Ihre gesamten Lebensversicherungsprämien bezahlen, fließt ein Teil des Geldes in den Abschluss einer Versicherung, ein Teil in die Gemeinkosten und den Gewinn der Versicherungsgesellschaft und ein Teil in die Provision des Verkäufers. Der Rest fließt dann in den Barwertteil der Police.

Jedes Jahr beschließt die Versicherungsgesellschaft eine Dividende. Wenn der Barwertanteil 10.000 US-Dollar beträgt und die Dividende 6 % beträgt, werden Ihrem Barwert 600 US-Dollar gutgeschrieben. Die Dividende wird nur auf den Barwert und nicht auf die gesamte gezahlte Prämie angewendet, sodass der durchschnittliche Dividendensatz in keiner Weise mit Ihrer tatsächlichen Rendite der Police als Investition zusammenhängt. Tatsächlich ist die Kapitalrendite im Allgemeinen mindestens ein Jahrzehnt lang negativ. Ich habe kürzlich eine Police für einen gesunden 30-jährigen Mann mit einer Lebenserwartung von 53 Jahren analysiert. Die garantierte Rendite auf den Barwert betrug NACH 5 JAHRZEHNTEN weniger als 2 % pro Jahr .

Selbst wenn Sie die optimistischen „prognostizierten“ Werte der Versicherungsgesellschaft verwenden, rechnen Sie immer noch mit einer Rendite von weniger als 5 %. In Wirklichkeit werden Sie am Ende wahrscheinlich eine Rendite von 3–4 % erzielen. Wenn man bedenkt, dass man diese „Investition“ fünf Jahrzehnte lang behalten muss, scheint das keine große Entschädigung zu sein. Wenn Sie Jahrzehnte zum Investieren haben, ist es weitaus klüger, mit Ihren Investitionen mehr Risiko einzugehen und eine höhere Rendite zu erzielen. Eine Investition in Aktien oder Immobilien dürfte über Jahrzehnte hinweg eine Rendite im Bereich von 7 % bis 12 % abwerfen. Aus 100.000 US-Dollar, die 50 Jahre lang mit 3 % pro Jahr investiert werden, werden 438.000 US-Dollar. Wenn es stattdessen um 9 % wächst, erhalten Sie am Ende 7,4 Millionen US-Dollar, also das 17-fache. Die Rate, mit der Sie Ihre langfristigen Investitionen aufzinsen, ist wichtig, insbesondere über lange Zeiträume.

Mythos Nr. 4 – Versicherungsunternehmen sind großartige Investoren

Einige Agenten glauben, dass Versicherungsunternehmen irgendwie Anlagerenditen erzielen können, die Sie oder ich anderswo nicht finden können, und diese großartigen Renditen an ihre Versicherungsnehmer weitergeben können. Es kann aufschlussreich sein, unter die Haube zu schauen und zu sehen, was sich wirklich im Portfolio einer Versicherungsgesellschaft befindet. Im Jahr 2016 wurden die Vermögenswerte der Versicherungsgesellschaften zu 67 % in Anleihen (fast ausschließlich in gewöhnliche Unternehmens- und Staatsanleihen), 1 % in Vorzugsaktien, 12 % in Stammaktien, 8 % in Hypotheken, 1 % in Immobilien, 4 % in Bargeld, 2 % in Darlehen an ihre Versicherungsnehmer und etwa 5 % in „Sonstiges“ investiert. Dank der Indexfonds-Revolution kann ein einzelner Anleger fast alles für weniger als 10 Basispunkte pro Jahr an Kosten kaufen. Aktives Management funktioniert für Versicherungsunternehmen nicht besser als für Investmentfonds.

Wie zu erwarten ist, sind die Renditen eines Portfolios, das hauptsächlich aus Staatsanleihen (derzeit mit einer Rendite von 1–2 %) und Unternehmensanleihen (derzeit mit einer Rendite von 3–4 %) besteht, nicht besonders hoch. Woher kommen also Dividenden? Ein Teil stammt aus der Rendite des Anlageportfolios, ein Teil stammt aus den Gebühren derjenigen, die ihre Policen gekündigt haben, und ein Teil stammt aus „Sterblichkeitsgutschriften“, bei denen es sich im Grunde um Geld handelt, das sie nicht an die Begünstigten auszahlen mussten, weil weniger Menschen starben als geplant (d. h. Sie haben aufgrund staatlicher Vorschriften von vornherein zu viel für den Versicherungsteil der Police bezahlt). Es gibt keine magischen Investitionen, in die Versicherungsunternehmen investieren können und die Sie ohne das Unternehmen nicht tun könnten. Jede zusätzliche Schicht zwischen Ihnen und der Investition erhöht lediglich die Kosten und verringert die Rendite.

Mythos Nr. 5 – Das ganze Leben ist eine großartige Anlageklasse

Es gibt viele Anlageklassen, die es wert sind, in ein diversifiziertes Portfolio aufgenommen zu werden, aber das ganze Leben gehört nicht dazu. Versicherungsvertreter greifen im Allgemeinen auf dieses Argument zurück, wenn sie erkennen, dass sie Sie nicht davon überzeugen können, dass das ganze Leben an sich eine großartige Investition ist. Sie sagen, dass es das Gesamtportfolio verbessert, wenn man es in ein Portfolio aus Aktien, Anleihen und Immobilien mischt. Sie können jedoch alles, was Sie wollen, als Anlageklasse bezeichnen. Pferdemist kann eine Anlageklasse sein, aber das bedeutet nicht, dass Sie darin investieren sollten. Stellen Sie es sich so vor. Wenn ich Ihnen sagen würde, dass ich eine Anlageklasse mit den folgenden Merkmalen habe:

- 50 % Frontload im ersten Jahr

- Übergabestrafen, die jahrelang anhalten

- Erfordert fortlaufende Beiträge über Jahrzehnte

- Es ist schwierig, ein Gleichgewicht mit anderen Anlageklassen herzustellen

- Abgesichert durch die Garantien eines einzelnen Unternehmens (und alles, was Sie von einer staatlichen Garantievereinigung erhalten können)

- Sie müssen Zinsen zahlen, um an Ihr Geld zu kommen

- Garantierte negative Renditen für das erste Jahrzehnt

- Geringe Rendite, selbst wenn man es über Jahrzehnte hält

- Muss lebenslang gehalten werden, um selbst eine geringe Investitionsrendite zu erzielen

- Ausgenommen von der Investition bei schlechtem Gesundheitszustand oder gefährlichen Hobbys

Würdest du es kaufen? Natürlich nicht.

Mythos Nr. 6 – Das ganze Leben ist eine großartige Möglichkeit, Steuern zu sparen

Nicht das ganze Leben ist der beste Weg, um Ihre Investitionssteuer zu senken, sondern Rentenkonten schon. Viele Makler preisen gerne die Steuervorteile einer Lebensversicherung und vergleichen sie oft mit einer 401(k) oder einer Roth IRA. Der Barwert wächst auf steuergeschützte Weise, der Barwert kann steuerfrei geliehen werden und die Erlöse aus der Police sind bei Ihrem Tod einkommenssteuerfrei (jedoch nicht erbschaftssteuerfrei). Einige Befürworter der Lebensversicherung schlagen daher vor, eine Lebensversicherung anstelle eines Rentenkontos wie 401(k) oder Roth IRA abzuschließen. Ein 401(k)- oder Roth-IRA bietet jedoch nicht nur MEHR Steuerersparnisse und ermöglicht Ihnen die Investition in risikoreichere Anlagen, die Ihnen wahrscheinlich eine höhere Rendite einbringen, sondern Sie müssen sich für das Privileg, dies zu tun, auch kein eigenes Geld leihen oder Zinsen zahlen.

Ich habe zuvor über die drei Möglichkeiten geschrieben, wie Sie mit einem 401(k) Steuern sparen können, und darüber, warum eine Lebensversicherung nicht mit einer Roth-IRA vergleichbar ist. Ich habe auch darüber geschrieben, dass steuereffiziente Investitionen in ein steuerpflichtiges Anlagekonto nicht annähernd die Steuerlast mit sich bringen, die Ihnen die Makler gerne erzählen. Gibt es Steuervorteile bei der Investition in eine Lebensversicherung? Ja, aber sie sind dramatisch überverkauft.

Mythos Nr. 7 – Eine Lebensversicherung schützt Ihr Geld vor Gläubigern

Versicherungsagenten nutzen diese Möglichkeit gerne bei Ärzten, die in Bezug auf Vermögensschutzfragen paranoid sein können. Allerdings erwähnen sie oft nicht (oder wissen es vielleicht gar nicht), dass Vermögensschutzgesetze sehr bundeslandspezifisch sind. Zum Beispiel [2022] In Alabama sind nur 500 US-Dollar des gesamten Barwerts einer Lebensversicherung vor Gläubigern geschützt, aber 100 % des Geldes in Ihrem 401(k) oder IRA sind geschützt. West Virginia bietet nur einen Schutz von 8.000 US-Dollar. South Carolina schützt 4.000 US-Dollar. New Hampshire bietet keinen Schutz. Viele Bundesstaaten bieten 100 % Schutz für den gesamten Barwert einer Lebensversicherung, aber Sie sollten sich wahrscheinlich über die spezifischen Gesetze Ihres Bundesstaats informieren, bevor Sie auf diesen Mythos hereinfallen.

Mythos Nr. 8 – Für die Nachlassplanung braucht man das ganze Leben

Eine Lebensversicherung mit Barwert bietet einige großartige Nachlassplanungsfunktionen, die sehr nützlich sein können. Die überwiegende Mehrheit der Menschen, darunter auch Ärzte, benötigt diese Funktionen jedoch nicht. Der Hauptvorteil einer Lebensversicherung besteht darin, dass Sie bei Ihrem Tod eine Menge einkommenssteuerfreies Bargeld erhalten. Dies kann bei vielen Liquiditätsproblemen hilfreich sein, beispielsweise beim Besitz einer teuren Immobilie oder eines Privatunternehmens. Wenn Sie zwei Kinder haben, die Sie zu gleichen Teilen an Ihrem Nachlass teilen möchten, und der Großteil Ihres Nachlasses der Familienbauernhof ist, müssten sie entweder den Bauernhof verkaufen, ihn halbieren oder einen anderen aufkaufen lassen, um ihn zu gleichen Teilen zu teilen. Wenn Sie jedoch auch eine Lebensversicherung mit dem gleichen Wert wie der Hof hätten, könnte ein Kind den Hof bekommen und das andere könnte den Versicherungserlös bekommen. Ebenso kann der Lebensversicherungserlös für die Zahlung der Erbschaftssteuern verwendet werden, wenn Sie über ein sehr großes Vermögen verfügen (mehr als 5 Millionen US-Dollar für Alleinstehende in der Bundessteuergesetzgebung, in einigen Bundesstaaten jedoch auch deutlich weniger). Dies wäre auch bei einem einzigen Erben nützlich, um zu verhindern, dass er eine wertvolle Immobilie oder ein Unternehmen zu Schnäppchenpreisen verkauft, um die Steuerschuld zu bezahlen.

Manche Leute schließen auch gerne eine Lebensversicherung in einem unwiderruflichen Trust ab, um die Größe ihres Nachlasses zu verringern und Erbschaftssteuern zu vermeiden. Während Sie stattdessen auch einfache steuerpflichtige Investitionen in den Trust investieren können (und aufgrund höherer Renditen wahrscheinlich die Nase vorn haben würden), können die Treuhandsteuersätze recht hoch sein, was die Rendite steuerineffizienter Investitionen erheblich schmälert, ganz zu schweigen vom Aufwand. Es ist wichtig darauf hinzuweisen, dass es nicht an der Lebensversicherung liegt, die Geld bei der Erbschaftssteuer spart, sondern an der Tatsache, dass Sie Ihr Vermögen vor Ihrem Tod verschenken, indem Sie es in den Trust einzahlen.

Tatsache ist jedoch, dass die überwiegende Mehrheit der Amerikaner, selbst Ärzte und sogar Ärzte mit einem „Erbschaftssteuerproblem“, keine Lebensversicherung benötigen, um eine effektive Nachlassplanung durchzuführen. Die meisten Menschen werden ohne Erbschaftssteuerbelastung sterben. Von denjenigen, deren Nachlässe Erbschaftssteuern schulden, verfügt die überwiegende Mehrheit über liquide Mittel, die zur Zahlung der Steuern verwendet werden können. Auch wenn Sie Ihren Nachlass verkleinern möchten, um Erbschaftssteuern zu vermeiden, können Sie dies problemlos tun, ohne eine Lebensversicherung abzuschließen. Sie und Ihr Ehepartner können jeweils 16.000 US-Dollar spenden [2022 – besuchen Sie unsere Seite mit den Jahreszahlen, um die aktuellsten Zahlen zu erhalten] an jeden Erben in einem bestimmten Jahr ohne Auswirkungen auf die Erbschafts-/Schenkungssteuer. Wenn Sie beispielsweise vier Kinder hätten und jedes davon vier Kinder hätte und alle 20 Erben verheiratet wären, wären das 40 Personen. 40 x 16.000 US-Dollar x 2 =1,28 Millionen US-Dollar pro Jahr, die aus Ihrem Nachlass entnommen werden können, ohne Erbschafts-/Schenkungssteuern zu zahlen. Bei diesem Steuersatz wird es nicht lange dauern, bis die Erbschaftssteuergrenze unterschritten ist, eine Versicherung ist nicht erforderlich.

Mythos Nr. 9 – Das ganze Leben ist eine großartige Möglichkeit, das Studium zu finanzieren

Einige Makler gehen sogar so weit, Ihnen vorzuschlagen, eine Lebensversicherungspolice abzuschließen, um das Studium Ihrer Kinder zu finanzieren. Können Sie das tun? Natürlich. Sie nehmen einfach ein Policendarlehen auf und überweisen das Geld an die Universität, um die Studiengebühren zu bezahlen. Aus mehreren Gründen ist es jedoch besser, mit guten 529 für das College zu sparen. Erstens erhalten Sie häufig eine staatliche Steuervergünstigung, wenn Sie eine 529-Karte verwenden, die für die Lebensversicherung nicht verfügbar ist. Zweitens müssen Sie sich kein Geld von Ihrem 529 leihen, sondern können es einfach abheben. Keine Zinszahlungen erforderlich. Berücksichtigen Sie zu guter Letzt den Zeitrahmen für die College-Ersparnisse. Eltern sparen in der Regel über einen Zeitraum von 5 bis 20 Jahren für das Studium. Wenn sie dieses Geld aggressiv investieren, können sie mit einer Rendite von 7–10 % rechnen. Lebensversicherungen bieten für Zeiträume von weniger als 20 Jahren sehr schlechte Renditen. Tatsächlich ist die Barrendite Ihrer „Investition“ im gesamten Leben oft mindestens ein Jahrzehnt lang negativ. Es ist wichtig, sicherzustellen, dass Ihr Geld genauso hart arbeitet wie Sie, und dass Ihr Geld im ersten Jahrzehnt einer lebenslangen Police im Urlaub ist. Befürworter des Lebensversicherungsschutzes werden darauf hinweisen, dass die Sterbegeldleistung im Falle Ihres Todes immer noch für das Junior-College bezahlt werden könnte, es jedoch weitaus günstiger ist, dieses Risiko mit einer Risikolebensversicherung abzudecken.

Mythos Nr. 10 – Das ganze Leben ist ein Luxus, den man sich wünscht

Versicherungsvertreter greifen gelegentlich auf dieses Argument zurück, wenn darauf hingewiesen wird, dass ein Kunde eigentlich keinen Bedarf an einer dauerhaften Sterbegeldleistung hat. Sie geben zu, dass der Kunde eigentlich keine Lebensversicherung benötigt. Dann versuchen sie es zu verkaufen, weil es ein Statussymbol oder Luxus ist. „Klar, das braucht man nicht, das ist ein Luxus.“ Ein Luxus ist per Definition etwas, das man nicht braucht. Ich bevorzuge, dass mein Luxus etwas ist, das ich wirklich genieße. Bevor Sie also eine Lebensversicherung als Luxus kaufen, fragen Sie sich:„Was macht mir wirklich Spaß?“ Wenn es sich um eine Lebensversicherung handelt, ist es gut, eine solche zu kaufen. Aber ich wette, die meisten von uns würden einen Luxus wie ein schönes Auto, eine Kreuzfahrt mit den Enkelkindern oder vielleicht eine Spende an eine beliebte Wohltätigkeitsorganisation bevorzugen.

Mythos Nr. 11 – Das ganze Leben ermöglicht es Ihnen, Ihr übriges Vermögen aufzubrauchen und bietet so wertvolle Flexibilität im Ruhestand

Das ganze Leben ist nicht der beste Weg, um sicherzustellen, dass Ihnen das Geld nicht ausgeht. Die Rente für einen Teil Ihres Vermögens ist jedoch die beste. Das ganze Leben ist nicht der beste Weg, um mit der Zweittod-Problematik umzugehen, wohl aber die richtige Strukturierung von Renten und Renten. Lebensversicherungsmakler entwickeln gerne Ruhestandsszenarien, die Ihnen das Gefühl geben, eine dauerhafte Lebensversicherung besitzen zu müssen oder zumindest besitzen zu wollen, insbesondere für ein verheiratetes Paar. Man spricht zum Beispiel von einer Rente, die nur bis zum Tod des berufstätigen Ehepartners ausgezahlt wird. Oder sie sprechen davon, einen Teil Ihres Vermögens auf der Grundlage des Lebens nur eines Mitglieds des Paares zu verrenten. Dann schlagen sie vor, dass der Erlös aus der gesamten Lebensversicherung für den Lebensunterhalt des vorletzten Ehegatten verwendet werden soll. Es gibt keinen Grund, eine Lebensversicherung auf diese Weise abzuschließen. Wenn Sie möchten, dass Ihre Rente bis zum Tod beider reicht, wählen Sie diese Option. Wenn Sie möchten, dass Ihre Rente so lange läuft, bis Sie beide sterben, dann wählen Sie diese Option. Ja, die Auszahlung erfolgt zu einem etwas geringeren Prozentsatz, aber die Differenz zwischen den Auszahlungen ist geringer als die Kosten einer Lebensversicherung, die den Verlust dieser Rente abdecken würde. Es ist einfach nicht die richtige Lösung für das Problem. Bietet eine Lebensversicherung eine gewisse Flexibilität im Ruhestand? Sicher, aber der Preis für diese Flexibilität ist zu hoch.

Mythos Nr. 12 – Das ganze Leben ist eine großartige Möglichkeit, teure Dinge zu kaufen

Das ganze Leben ist nicht der beste Weg, teure Dinge zu kaufen, dafür aber zu sparen. Es gibt einige wirklich kreative Versicherungsvertreter, die sich für Systeme wie Bank on Yourself oder Infinite Banking einsetzen. Das Grundprinzip ist folgendes:Durch die entsprechende Strukturierung Ihrer Police mit eingezahlten Zusätzen erhalten Sie in den ersten Jahren einen hohen Barwert in Ihre Police, sodass Sie in 3–4 Jahren statt in 8–15 Jahren die Gewinnschwelle erreichen. Sie kaufen auch eine Police mit „nicht direkter Anerkennung“. Das bedeutet, dass die Versicherungsgesellschaft beim Ausleihen von der Police weiterhin Dividenden auf den Betrag auszahlt, der vor der Ausleihe vorhanden war, sodass die Policendividenden im Wesentlichen die für das Darlehen fälligen Zinszahlungen aufheben. Anstatt jetzt auf Ihr Sparkonto oder zu einer Bank zu gehen, um sich Geld zu leihen, wenn Sie ein Auto, einen Kühlschrank oder eine als Finanzinvestition gehaltene Immobilie benötigen, können Sie praktisch kostenlos Kredite aus Ihrer gesamten Lebensversicherung aufnehmen. Darüber hinaus wächst der Barwert der Police, die Sie nicht leihen, schneller als das Geld auf einer Sparkasse.

Was ist also das Problem? Das Problem besteht darin, dass Sie eine Lebensversicherung abschließen müssen, die Sie nicht benötigen. Möglicherweise erreichen Sie die Gewinnschwelle früher als bei einer herkömmlichen Police, aber es gibt immer noch mehrere Jahre mit negativen Renditen und auf lange Sicht die gleichen niedrigen Renditen. Ist es besser, nach 5 Jahren 4–5 % pro Jahr zu verdienen oder ab Jahr 1 1 % pro Jahr zu verdienen? Nun, in den ersten 6 oder 7 Jahren sind Sie mit dem 1 %-Sparkonto pro Jahr besser dran. Auch wenn die Zinssätze von ihren historischen Tiefstständen steigen, sind Sie immer noch für den Rest Ihres Lebens an dieses System gebunden. Es ist noch nicht lange her, dass ich aus einem Geldmarktfonds mehr als 5 % herausholen konnte. Außerdem scheint es sehr einfach zu sein, ein Auto zu extrem niedrigen Zinssätzen beim Händler zu finanzieren. 0 % oder 1 % sind keine Seltenheit. Es ist besser, bei ihnen einen Kredit zu 1 % aufzunehmen, als bei Ihrer Police zu 5 %. Ein ähnliches Problem besteht bei Haushaltsgeräten und Hypotheken. Man macht sich all diese Mühen, um sich selbst etwas zu leihen, und stellt dann fest, dass es günstiger ist, etwas von jemand anderem zu leihen. Und schließlich:Wenn Sie fünf oder zehn Jahre lang keinen Kauf tätigen müssen, haben Sie Zeit, in etwas zu investieren, das wahrscheinlich eine viel höhere Rendite bringt als eine Lebensversicherungspolice. Werden diejenigen, die auf sich selbst vertrauen, betrogen? Nicht unbedingt, aber die Vorteile ihres Programms werden ihnen im Allgemeinen überschätzt. Seine Befürworter sind in erster Linie Versicherungsmakler, die durch kreatives Marketing ihre Umsätze steigern wollen. Sparen ist einfach eine bessere Möglichkeit, große Anschaffungen zu tätigen, als eine lebenslange Police abzuschließen.

Mythos Nr. 13 – Wirklich reiche Leute oder Unternehmen schließen eine Lebensversicherung ab, also sollten Sie das auch tun

Befürworter der Lebensversicherung, insbesondere diejenigen, die dafür plädieren, Ihre Police als Bank zu nutzen, weisen gerne darauf hin, dass viele sehr wohlhabende Menschen und viele Unternehmen (einschließlich Banken) tatsächlich eine Lebensversicherung abschließen. Obwohl dies wahr ist, ist es für den Durchschnittsmenschen irrelevant. Große Unternehmen haben keinen Zugang zu den steuersparenden Rentenkontooptionen, die Mittelschichtsbürgern bieten. Ultrareiche Personen haben diese bereits ausgeschöpft. Wenn Sie viel mehr Geld haben, als Sie jemals brauchen können, ist die Rendite Ihres Geldes nicht so wichtig. Bill Gates kann es sich leisten, in etwas zu investieren, das eine Rendite von 2–5 % bringt, weil er sein Geld nicht braucht, um sehr hart zu arbeiten. Das gilt einfach nicht für die überwiegende Mehrheit der Menschen der Mittel- und Oberschicht, einschließlich Ärzten. Wie oben erläutert, profitieren besonders wohlhabende Menschen auch eher von den begrenzten Nachlassplanungsvorteilen und Vermögensschutzvorteilen einer dauerhaften Lebensversicherung. Kurz gesagt, die geringen Erträge, die das ganze Leben mit sich bringt, sind für sie viel weniger ein Problem als für Sie.

Mythos Nr. 14 – Man sollte sich das ganze Leben kaufen, wenn man jung ist

Verkäufer von Lebenslebensversicherungen weisen gerne darauf hin, dass Lebenslebensversicherungen viel günstiger sind, wenn man sie in jungen Jahren kauft. Es stimmt zwar, dass die Prämien niedriger sind, wenn Sie eine Police mit 25 Jahren kaufen, als wenn Sie sie mit 55 Jahren kaufen. Berücksichtigt man jedoch den Zeitwert des Geldes und die Tatsache, dass Sie die Prämien für drei weitere Jahrzehnte zahlen, ist die Investition in jungen Jahren nicht besser als in höheren Jahren. Versicherungsmathematiker sind sehr intelligente Menschen, und für ein Risiko, das relativ einfach zu modellieren ist, wie zum Beispiel den Tod, können sie Versicherungspreise recht effizient festlegen.

Abgesehen von den niedrigeren Prämien gibt es zwei weitere Gründe, warum es besser erscheint, es zu kaufen, wenn man jung ist. Erstens wird diese Provision auf mehrere Jahre verteilt, sodass sie weniger Auswirkungen auf Ihre Gesamtrendite hat. Weitaus attraktiver ist jedoch die Alternative, die Provision gar nicht zu zahlen. Zweitens ist es möglich, dass Ihre Gesundheit abnimmt oder Sie später im Leben einer gefährlichen Sportart nachgehen. Dies ist einer der gravierenden Nachteile der Lebensversicherung als Kapitalanlage – nicht jeder kann sie nutzen. Entweder qualifizieren sie sich überhaupt nicht dafür, oder der Versicherungspreis ist so hoch, dass die Rendite der Investition noch niedriger ist, als sie es sonst wäre. Ich sehe das nicht als einen Grund, es zu kaufen, wenn man jung ist, sondern als einen Grund, es überhaupt nicht zu kaufen. Können Sie sich vorstellen, dass Vanguard einen Sanitäter zu Ihnen nach Hause schickt, um Blut abzunehmen, bevor Sie den S&P 500-Fonds kaufen dürfen?

Mythos Nr. 15 – Der Verzicht auf Premium-Fahrer ist eine gute Möglichkeit, Ihren Ruhestand vor Ihrer Invalidität zu schützen

Eine Lebensversicherung ist nicht der beste Weg, um Ihr Ruhestandseinkommen vor Ihrer Invalidität zu schützen, sondern eine Invalidenversicherung. Da die Versicherungsgesellschaften erkannten, dass die Prämien für eine Lebensversicherung sehr teuer sind und es schwierig wäre, sie im Falle einer Invalidität zu erhalten, haben sie damit begonnen, einen Fahrer anzubieten, der im Falle einer Invalidität auf die Prämien verzichtet. Manchmal scheint es, als müssten Sie für diesen Vorteil nicht einmal extra bezahlen. Wer auf diese Taktik hereinfällt, verpasst ein paar Punkte. Erstens sind Garantien nicht kostenlos. Jede Garantie kostet Sie Geld in Form einer geringeren Rendite, unabhängig davon, ob die Versicherungsgesellschaft einen Aufpreis für die Garantie berechnet oder sie „in die Police integriert“, sodass sie verborgen bleibt.

Zweitens ist die Invaliditätsversicherung kompliziert und die Definition von Invalidität ist von entscheidender Bedeutung. Die meisten Ärzte, die eine Berufsunfähigkeitsversicherung wünschen, geben viel Geld aus, um eine wirklich gute Police mit einer breiten Definition von Berufsunfähigkeit abzuschließen, die auch eine „Eigenberufsversicherung“ einschließt, weil sie sicherstellen wollen, dass das Unternehmen im Falle ihrer Berufsunfähigkeit aufkommen muss. Die im Rahmen von Lebensversicherungen verkauften Mitfahrer sind bei weitem nicht so umfassend und werden in den vielen Grauzonen, in die Behinderungen oft fallen, weitaus seltener bezahlt. Sie werden mit ziemlicher Sicherheit besser dran sein, eine umfangreichere Invaliditätsversicherung abzuschließen, als eine lebenslange Befreiung von der Prämienversicherung. Ihre Berufsunfähigkeitsversicherung bietet möglicherweise auch einen Altersvorsorgeschutz an. Auch wenn diese Probleme mit sich bringen (hauptsächlich in Bezug auf die Art und Weise, wie die Leistung ausgezahlt wird), sind sie besser als der Versuch, eine Berufsunfähigkeitsversicherung über eine Lebensversicherung abzuschließen.

Wenn Sie wie ich eine vorzeitige Pensionierung planen, stellen Sie möglicherweise fest, dass Sie Ihre Berufsunfähigkeitsversicherung ohnehin nicht benötigen, um Ihre Rentenbeiträge abzusichern, zumindest nach einigen Jahren mit hohen Ersparnissen. Erwägen Sie, im Alter von 40 Jahren ein Portfolio von 750.000 US-Dollar zu haben. Sie gehen davon aus, dass Sie in heutigen Dollars 2 Millionen US-Dollar für den Ruhestand benötigen. Sie planen, viel zu sparen, damit Sie das im Alter von 50 Jahren erreichen und in Rente gehen können. Was ist der Ersatzplan, wenn Sie arbeitsunfähig werden und nicht das ganze Geld sparen können? Ihre Berufsunfähigkeitsversicherung zahlt nicht nur bis zum Alter von 50 Jahren, sondern auch bis zum Alter von 65 Jahren. Sie benötigen also nicht, dass Ihr Portfolio diese 15 Jahre abdeckt. Sie können auch mit dem Bezug von Sozialversicherungsbeiträgen beginnen, wenn die Invaliditätsbeihilfen auslaufen. Da Sie Ihr Portfolio nicht anfassen müssen, kann es weiter wachsen. Wenn es nach der Inflation um 5 % wächst, wird es im heutigen Dollar über 2,5 Millionen US-Dollar wert sein, wenn Sie 65 Jahre alt werden. Kaufen Sie keine Versicherung, die Sie nicht brauchen. Aber noch bevor Sie überhaupt ein Portfolio haben, ist der beste Weg, Ihre Altersvorsorge zu schützen, der Abschluss einer MEHR Berufsunfähigkeitsversicherung und nicht der Versuch, diese aus einer Lebensversicherung zu erhalten. Auch wenn Sie die zusätzliche Absicherung für die Altersvorsorge nutzen könnten, müssen Sie in der Lage sein, sie in eine Anlage mit einer hohen Rendite zu stecken, die das ganze Leben wahrscheinlich nicht bringt. Ein aggressiv angelegtes steuerpflichtiges Konto ist völlig in Ordnung, da Ihr Haupteinkommen im Falle einer Erwerbsunfähigkeit, Ihre Leistungen aus der Erwerbsunfähigkeitsversicherung, steuerfrei sind.

Mythos Nr. 16 – Sie sollten Ihre miese alte Lebensversicherungspolice gegen eine glänzende neue eintauschen

Da ein Makler jedes Mal eine neue Provision erhält, wenn er eine neue Police verkauft, selbst wenn er eine alte Police desselben Unternehmens ersetzt, besteht für ihn ein ernsthafter Interessenkonflikt, wenn es darum geht, Ihnen Empfehlungen zu geben. Ich interagiere in diesem Blog mit vielen Versicherungsvertretern, und keiner von ihnen stimmt mit den anderen darüber überein, was eine „richtig strukturierte“ Lebensversicherungspolice ist. Das heißt, wenn Sie sich an einen zweiten Agenten wenden, wird dieser Ihnen mit ziemlicher Sicherheit sagen, dass es einen besseren Weg gibt, dies zu tun. Damit es sich jedoch lohnt, eine Police gegen eine andere auszutauschen, muss die ursprüngliche Police absolut schrecklich sein, insbesondere nach ein paar Jahrzehnten. Der Grund dafür ist, dass sich die schlechten Renditen der Lebensversicherung auf die Anfangsjahre konzentrieren. Ich habe mir kürzlich eine Police angesehen. Dies wurde als Kapitalanlage mit eingezahlten Zuschüssen für die ersten 25 Jahre angelegt. Es war der beste Versuch des Maklers, die Rendite einer Police zu maximieren. So sahen die annualisierten Renditen aus:

Garantiert Prognostiziert Erste 10 Jahre-1,84 %0,98 %Nächste 15 Jahre2,55 %5,47 %Nächste 25 Jahre1,99 %5,13 %Dies zeigt, dass sich die schlechten Renditen stark auf die Anfangsjahre konzentrieren. Bei dieser speziellen Police sinken die Renditen tatsächlich nach 25 Jahren, da dann keine eingezahlten Zuzahlungen mehr getätigt werden. Bei einer traditionelleren Police wäre die dritte Reihe etwas höher als die zweite Reihe. Aber die Moral der Geschichte ist, dass Sie zuerst die „richtige Police“ kaufen sollten, und selbst eine beschissene Police, die mehr als 10 Jahre alt ist, wird besser sein als eine brandneue, bessere Police. Dies ist auch der Grund dafür, dass es sinnvoll sein kann, eine ältere Lebensversicherungspolice beizubehalten, selbst wenn der Kauf ein Fehler war. Es ist auch bemerkenswert, wie wenig Risiko die Versicherungsgesellschaft tatsächlich eingeht, da sie nicht einmal garantiert, dass Ihr Barwert mit der Inflation Schritt hält.

Mythos Nr. 17 – Das ganze Leben ist die einzige Möglichkeit, Geld einkommenssteuerfrei an die Erben weiterzugeben

Das ganze Leben ist nicht die einzige Möglichkeit, bei Ihrem Tod Geld einkommenssteuerfrei an die Erben weiterzugeben. Tatsächlich ist es nicht einmal der beste Weg, eine Roth IRA ist es. Wenn Sie sterben, erhalten Ihre Erben eine einkommensteuerfreie Sterbegeldversicherung. Was Makler oft nicht erwähnen, ist, dass nahezu alles, was Ihre Erben nach Ihrem Tod von Ihnen bekommen, einkommenssteuerfrei ist. Dank der Erhöhung der Bemessungsgrundlage im Todesfall wird alles, was nicht über ein Rentenkonto verfügt, einschließlich Möbel, Autos, Aktien, Bargeld, Investmentfonds und Immobilien, am Tag Ihres Todes neu bewertet. Da die Basis nun mit dem Wert übereinstimmt, fallen keine Kapitalertragssteuern an. Noch besser kann es sein, ein Rentenkonto zu erben, insbesondere ein Roth-Konto, bei dem die Steuern bereits gezahlt wurden. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

Myth #18 — With Whole Life, There Is No Way I Can Lose Money

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

Myth #19 — Life Insurance Should Not Be “Rented”

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

Myth #20 — Banks Own Life Insurance So You Should Too

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Myth #21 — Corporate CEOs Own Whole Life Insurance So You Should Too

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

Myth #22 — Banks Failed During The Great Depression, But Insurance Companies Didn't

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

Myth #23 — After-Tax, Whole Life Returns Are Better Than Bond Returns

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

Myth #24 — Whole Life Insurance Keeps Assets Off the FAFSA

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Myth #25 — Term Life Expires Without Paying Anything

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

Myth #26 — Whole Life Insurance Is the Perfect Investment

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

#1 Safe

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

#2 Liquid

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

#3 Tax-Advantaged

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

#4 Creditor-Proof

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

#5 Competitive Return

Are you kidding me? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

- Guaranteed negative return for years

- Requirement to interact with and pay a commission to an insurance agent

- Requirement to give samples of body fluids and submit to a medical exam

- Requirement to answer pesky questions about my health

- Requirement to avoid risky activities

- Requirement to pay interest in order to use my own money

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

Myth #27 — Insurance Agents Are Just People

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

Myth #28 — No 1099 Income with Whole Life

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Myth #29 — What Does The White Coat Investor Know? He's Just a Doctor, and Probably a Crappy One

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

Myth #30 — After Maxing Out a 401(k) and Roth IRA, Isn't Whole Life Insurance the Only Tax-Sheltered Option Left?

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

Myth #31 — The Estate Tax Exemption Could Go Down

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

Myth #32 — Whole Life Insurance Protects from Nursing Home Creditors

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

- Your home if your spouse lives in it

- The value of one vehicle (including a Tesla)

- Funds set aside for a funeral

- Household and personal items

- Cash value of your life insurance policies IF the total face value of all policies is <$1500

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

Myth #33 — WCI Doesn't Understand the Opportunity Cost of Borrowing Against Whole Life Insurance and Investing Elsewhere

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

Myth #34 — Buy Whole Life Insurance for the Long Term Care Rider

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

Myth #35 — We Don't Say Put All Your Money into Whole Life Insurance

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

Myth #36 — Yes, We Have a Few Bad Eggs But Most of Us Are Ethical

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

Myth #37 — You Should Buy Insurance to Preserve Insurability

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

Myth #38 — Whole Life Insurance Is a Great Investment to Put in Your Defined Benefit/Cash Balance Plan

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

Myth #39 — More Money Is Passed Through Life Insurance

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

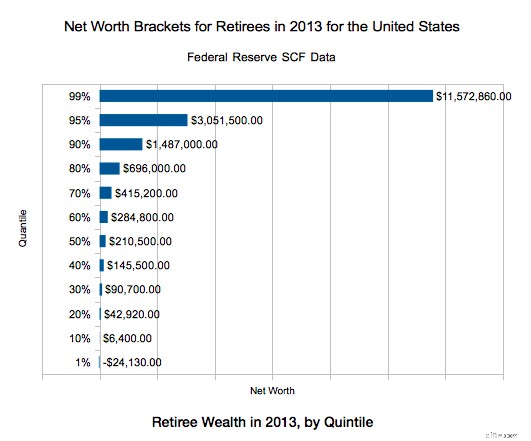

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

- The average retired adult who dies in their 60s leaves behind $296K in net wealth,

- $313K in their 70s, $315K in their 80s

- $283K in their 90s

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

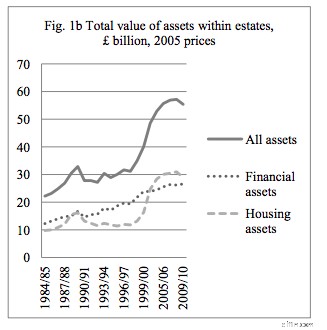

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

Myth #40 — You Get an Investment and Life Insurance

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Summing It Up

Los geht's. Forty reasons for buying whole life insurance debunked. Mach dir keine Sorge; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

- Need or desire a guaranteed, but possibly slowly increasing, life-long death benefit,

- Understand that the guarantee/contract essentially relies on the insurance company staying in business for as long as he lives for any policy of reasonable size,