Siehe Mein Budget:Ich lebe Vollzeit in einem Wohnmobil

Möchten Sie in das Vollzeit-Wohnmobilleben eintauchen, fragen sich aber die Details der Finanzen? Sehen Sie, wie eine Vollzeit-RVer, die das Land bereist, das Beste aus ihren monatlichen Zuflüssen macht, ohne ihre finanziellen Ziele zu opfern.

Über

- Name: Der Wanderer

- Alter: 38

- Standort: Mit dem Wohnmobil durch die Nationalparks des Landes

- Arbeit: Instructional Designer &Business Owner

- Wohnsituation: Single und seit 18 Monaten allein in einem Wohnmobil lebend

Einkommen:89.000 $+/Jahr (je nach Geschäft variabel)

- Tagesjob:66.000 $/Jahr

- Invalidenrente für Veteranen:14.000 $/Jahr

- Geschäftseinkommen:$9.000+/Jahr. Dies ändert sich schnell. Das Geschäft läuft hoch, ist aber in Bewegung und kommt in Gang. Ich schätze, ich werde dieses Jahr 50.000 $ verdienen.

Einsparungen:53.000 $

- Ich habe die Auszahlung vom Haus im Rahmen der Scheidung erhalten. Als ich vor 18 Monaten ging, hatte ich 400 $ auf einem Girokonto und das war's.

- Vor der Auszahlung vor zwei Monaten hatte ich normalerweise etwa 5.000 $ auf meinem Konto.

Schulden:62.500 $

- Anhänger:31.500 $ (bei 4,3 % Zinsen)

- Lkw:31.000 $ (bei 3,6 % Zinsen)

Ich überlegte, meine Kredite zurückzuzahlen, als die Zahlung für das Haus eintraf, aber nachdem ich mit einem weisen Freund gesprochen hatte, sagten sie, es wäre nett, mir mit diesem Geld alle Optionen offen zu halten. Ich sehe es also als FU-Geld an – es sind Ausgaben im Wert eines Jahres. Meine Nebenbeschäftigung läuft gut und dies könnte es mir ermöglichen, Vollzeit zu arbeiten.

Durchschnittlicher monatlicher Zufluss:$5.000+/Monat

- Tagesjob:3.163 $

- Veteranenvorteil:1.146 $

- Geschäftsgewinn:500 $ bis 4.000 $

Mein Budget

Ich bin seit dem 23. März 2020, dem Tag meines Auszugs, YNAber. Ich habe viele Kategorien, aber ich mag es, sie alle aufzuteilen, damit ich sehen kann, wie sich die Kosten aufschlüsseln.

Budget

| Kategorie | Zielbetrag | Notizen |

| Fixkosten | ||

NYT  | $5 | |

Google-Speicher  | $5 | |

Versicherung für Lagerraum  | $9 | |

LKW-Darlehen  | $556 | |

Crashplan  | $10 | Software-Computer-Backup |

Pandora  | $9 | |

Computertinte  | $3 | Abonnementdienst |

| Google Fi | $70 | Unregelmäßig. 48 bis 80 $ nach Nutzung bezahlt |

Wohnmobildarlehen  | $357 | |

Internet-Hotspot von Verizon  | $54 | Es ist wichtig, mehrere Internetanbieter zu haben, damit ich von überall arbeiten kann |

Speichereinheit  | $142 | |

| Internet-Hotspot von AT&T | $25 | Ich habe meine Seele verkauft und es hat sich für diesen Preis gelohnt. |

Spot  | $12 | Notsignal, damit ich alleine wandern gehen kann und nicht alleine sterben werde. |

RV-Versicherung  | $125 | Sie müssen eine spezielle Versicherung haben, wenn Sie ein Vollzeit-Wohnmobil sind. |

LKW-Versicherung  | $95 | |

| Lebensmittel &Rauschmittel | ||

Lebensmittel  | $250 | |

| Essen gehen | $50 | |

Alkohol und Weed  | $40 | Ich kaufe in großen Mengen in Colorado – definitiv das beste Preis-Leistungs-Verhältnis. |

| Allgemeine Ausgaben | ||

Campinggebühren  | $1.000 | Ich halte es bei 30 $/Nacht Durchschnittskosten zwischen BLM-Land, Freunden und öffentlichen und privaten Campingplätzen. |

RV-Wartung  | $100 | |

Haushaltswaren  | $100 | |

Diesel  | $600 | Liegt zwischen 50 $ und 800 $, je nachdem, wie weit ich fahre. |

| LKW-Wartung | $100 | |

Haarschnitt  | $30 | Ich schneide und schneide meine Haare selbst und gebe dann alle sechs Monate 200 $ in einem Salon aus, um professionelles Bleichen und Färben zu bekommen. |

| Kleidung | $100 | |

Porto  | $10 | Ich habe ein Postfach in Florida, um meine Post auf Reisen zu verwalten. |

| Hardware | $42 | Telefone, Computer, Ersatz |

Spiele/Bücher/Filme  | $5 | Ich habe 38 $ gespart. Vielleicht hole ich mir ein Kochbuch! |

| Vinyl | $40 | Neue Kategorie. Früher waren es Kreditkartenzinsen. Das habe ich in den Kauf von Platten übertragen. |

Outdoor-Ausrüstung und Zubehör  | $50 | Bisher 250 $ gespart. |

| Dienstleistungen und Tickets im Freien | $10 | Staatsparkgebühren |

| Veranstaltungstickets | $0 | Konzertkarten (wenn ich sie überhaupt mit Geld auffülle) |

Souvenirs of Life  | $50 | Dinge, die ich selbst bekomme, wenn ich die Nationalparks bereise. |

Geschenke  | $50 | |

Seltsame Scheiße  | $100 | Zeug, für das ich vergessen habe, ein Budget einzuplanen |

| Einsparungen | ||

Notfallfonds  | $110 | Die Bank schöpft alle paar Tage automatisch den Höchstbetrag ab, um beim Aufbau von Einsparungen zu helfen. Auch die Hausgeldauszahlung fällt in diese Kategorie. |

Ruhestand/Roth IRA  | $500 | Sparen bis zum Maximum meiner Roth IRA. |

| Jährliche Kosten (RV) | ||

| Gebühren für die Steuervorbereitung | $13 | Mein Leben wurde kompliziert genug, ich habe dieses Jahr einen Steuerberater bekommen. |

Gebühr für die Alaska Air Card  | $7 | |

Mail-Weiterleitung  | $16 | Ich bezahle 200 $/Jahr, damit meine E-Mails an mich weitergeleitet werden. |

AAA  | $10 | Und darf ich sie nie brauchen. |

Marcell  | $8 | Anhängerüberwachungs-App – Temperatur. Hilfreich, als ich meine Katze hatte. |

YNAB  | $7 | |

| Die Hochzeit des besten Freundes | $200 | Ich habe 600 $ gespart, aber ich werde sie bald ausgeben! |

Amazon  | $10 | |

| Steuern und Registrierung | $60 | |

| Scheidung | ||

Scheidungskosten  | $1.000 | Ich hoffe, das verschwindet bald. Aber das ist für meinen Anwalt. |

| Nebengeschäft | ||

| Einkommenssteuern (40 %) | $0 | Ich verfolge in den Notizen, wie viel ich hinzufügen muss, aber es variiert stark. Ich habe bisher 3500 $. |

| Adobe | $29 | |

| Gesamtbedarf $6.174 | ||

Expenses Specific to Full-Time RV Living

There are a bunch of things in my budget specific to full-time RV living:

- Special insurance. When you’re living full-time in an RV, you pay for more expensive insurance compared to a person who takes their RV out three times a year.

- A mailbox forwarding service. I use a mailbox in Florida as an address for packages and mail, and they forward me my stuff wherever I’m at.

- Three internet subscriptions. I have to be connected to do my job, and not all providers have equal coverage. That means I pay for a Verizon hotspot, an ATT hotspot, and I can hotspot off of FI.

- I use an app that shows a Wifi coverage map that I use frequently.

- It’s often worth it to stay in a nearby town for the wifi instead of always camping inside a park. Parks usually don’t have good enough reception for work. Sometimes, they have none. For the record, Death Valley has no service. Überhaupt. Plan accordingly.

Meine Geschichte

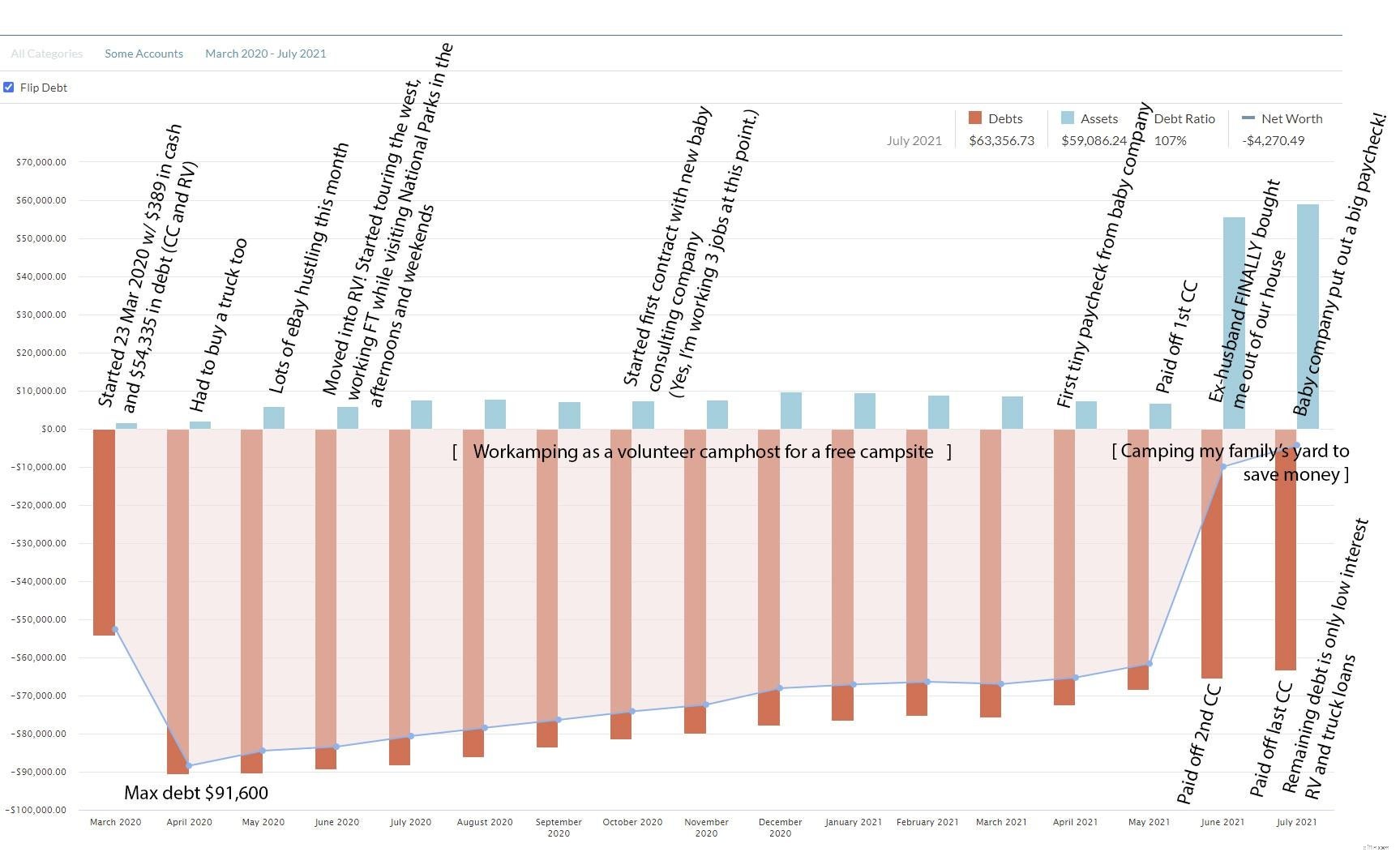

In late March 2020, when the world was shutting down, I finally called it quits on my marriage. Best decision I will make in my life. There were a lot of issues in our relationship, but the worst to me was his total disconnect and denial about spending within our limits. In five years, we spent $115k more than we brought in—burning through my $75k in pre-marriage savings and accruing $40k in credit card debts.

I moved out with less than $400 in the bank, almost $20k on credit cards (we split the $40k credit card debt equally), and assumed the responsibility for the loan on our one-year-old RV. He kept the house, the car, and the majority of our stuff. I just wanted out.

My plan was to move into the RV and travel the US seeing National Parks. In addition to the debt I already had, I had to buy $37k worth of a big diesel truck to make those dreams happen. I also needed to build an emergency fund.

I work for an educational non-profit making $66k/year and I get $1,100 a month in Veterans Disability Pay. That’s less than $4,800 a month in take-home pay. I wasn’t even making it paycheck to paycheck.

RV life isn’t cheap if you are on the move, so I cut my expenses down to the bare bones to make ends meet and started hustling hard:

- I worked full-time at my day job.

- Hustled stuff on eBay.

- Found a camp host gig for seven months in central California where I took care of a campground in exchange for a free site.

- Started a consulting business with a couple trusted friends that began work in October but didn’t start leaking out tiny profits until this April.

- I scrabbled tooth and nail for months to get my stimmies and tax refunds from the IRS who automatically flags anyone who changes their legal name (this problem is only an issue for women).

- There were unclaimed funds found from my dead grandmother being held by the state of Alaska.

- A lawyer was hired to get my ex-husband to finally pay me for my own house!

- I did everything I could to make money and pay down my debts.

With all that hustling and scrimping:

- I paid off $28,000 in just over a year.

- I’ve built up two months worth of expenses in my checking account

- I’ve built up another month of expenses in my emergency fund.

Between my hustling and the house settlement, it’s all about $87,000 total between paying off debt and cash saved since the divorce. That’s not counting my retirement funds, where I unintentionally managed to max out my 403b last year. Combined with a truly bumper year on the stock market for me, those accounts have increased about $80,000 as well in this time period.

I traveled to 26 National Parks (some multiple times), visited every member of my family across the West during a pandemic, lost 60 pounds, and generally just crushed it. I can’t give YNAB credit for the weight loss or the National Parks, but I can say it’s been the central tool in almost every decision I’ve made, kept me on course, allowed me to achieve so much more than I could have imagined in such a short time.

Thanks, YNAB, you’ve earned your $84.

Start your own free trial of YNAB, no credit card required.

Meine finanziellen Ziele

Before my next birthday, I want to:

- Clear $100K from a single income source.

- Quit my day job.

- Reach the $250,000 in retirement accounts (I’m at $215K).

I follow a lot of FIRE stuff but I don’t think I actually want to quit and never work again because I like what I’m doing with my side business. I want to see it succeed.

Do I want to work my business 40 hours a week? No—I want to travel, quit my day job, and have the ability to generate income to support my lifestyle.

I don’t have goals to buy a house, I’ve been doing the RV thing for 15 months. I can see myself doing this for another three or four years. Maybe somewhere along the way I’ll meet someone who’s worth stopping for. Or, I’ll say OK cool, maybe not. And I’ll live overseas and travel Europe. Either way, it’ll work out.

Ich würde meine derzeitige finanzielle Situation mit 5/5

bewertenA Financial Counselor Reacts

I’m Rachel, a writer and an Accredited Financial Counselor® here at YNAB. I had the pleasure of talking to The Wanderer for this YNAB Snapshot.

First, I just cannot even put into words how impressive this turnaround has been. And in such a short amount of time! If I could just have an ounce of the wanderer’s grit…whew what could we even accomplish?!

I really liked hearing the thought process behind The Wanderer’s financial decisions. She really thinks through all angles and makes the choice that’s best for her situation:take the cash inflow and the outstanding debt, for example. Advice from other financial gurus might be to go headfirst, or four-legged-graceful-creature intense to knock out that debt. BUT, she’s choosing to keep it and keep her options open.

I really liked that, and I love that she’s making a bet on herself. The interest rates on the truck and RV are reasonable (sub 5%), and it’s also not unlike having a mortgage payment, as her RV/truck setup is her primary residence. Sure, it probably won’t appreciate like a house (though who knows…car prices are crazy this year), but thinking of the expense as an accepted sunk cost:I can get behind that.

For The Wanderer, I really had to dig to find something, I really like her budget setup, I like her approach to saving and maxing out those retirement accounts.

What matters more:earning an extra $200-$300 this year, or having a simplified bank account setup?

2. Is there any further way we could simplify your financial life? You’ve got three credit cards you just paid off (HUZZAH!!). What’s your plan there for keeping them open or closing them? If you get to a point where you don’t really need to take out a big loan in the next few years, consider closing two of the three and just leaving one open. By the way, what is your credit score?

Ok, then! It doesn’t get much better. Absolutely nothing to worry about there. Credit scores take a bit of a hit when you close down a line (or three) of credit, but honestly—the more you use YNAB, the more you realize credit scores aren’t as important as you might’ve believed. Buying a house or a business loan would be the exception:you want to keep that perfect score for a large loan like that. Each fraction of a point adds up there!

And with that, this money snapshot reaches its end. Who knows what The Wanderer will do next—rafting down the Grand Canyon? Driving Porsches on a test track? We’re not sure—but her Wish List is full so it’s just a matter of time before those things become a reality too.

Want to gain total control of your money? Get started with your own budget and make your full-time RV living dreams come true!

-

Ein Leitfaden für kleine Unternehmen zu flexiblen Budgets

Ein flexibles Budget kann eine nützliche Ressource für Geschäftsinhaber sein, die Schwierigkeiten haben, variable Kosten angemessen zu budgetieren. Wenn Sie Produkte herstellen, erfahren Sie, wie ein

-

5 Tipps für ein angenehmes Leben mit knappem Budget

Heutzutage spüren immer mehr Menschen die Not, aber Budgetierung muss kein Problem sein. Sehen Sie mehr Bankenbilder. Leider haben nur wenige Menschen auf diesem Planeten Zugang zu riesigen Vorräten

Budget

- Werbebudgetplanung für Ihr kleines Unternehmen

- Budgetkontrolle mit Kapitalrationierung

- Erstellen eines Finanzbudgets für Ihr Unternehmen

- 4 Tipps zur Unternehmensbudgetierung von den Profis

- Verpflichtung zu einem Cash-Budget für Ihr kleines Unternehmen

- Vorbereitung des Kapitalbudgets vor der Eröffnung Ihres eigenen Unternehmens

- Einen gesunden Lebensstil mit kleinem Budget führen

- 170.000 $ Haushaltseinkommen:Siehe unser Budget

- Sie benötigen ein separates Geschäftsbudget

-

Wintergarten-Ideen mit kleinem Budget:Sehen Sie, wie wir es gemacht haben

Wintergarten-Ideen mit kleinem Budget:Sehen Sie, wie wir es gemacht haben Du brauchst also ein paar Wintergarten-Ideen mit kleinem Budget, oder? Wir auch! Wir haben unseren Wintergarten mit einem Gesamtbudget von 15.000 $ gebaut:So haben wir es gemacht. Als wir in unser ...

-

So erstellen Sie ein Geschäftsbudget im Jahr 2022

So erstellen Sie ein Geschäftsbudget im Jahr 2022 Ein Geschäftsbudget kann Ihnen helfen, die Kosten unter Kontrolle zu halten und den Umsatz zu steigern. Erfahren Sie, wie Sie in fünf Schritten ein Geschäftsbudget für Ihr kleines Unternehmen erstelle...